The Muscle Problem: Who Controls the Actuators Controls the Robot

Actuators eat 40–60% of a humanoid's build cost — and the race to own that layer is rewriting the entire supply chain.

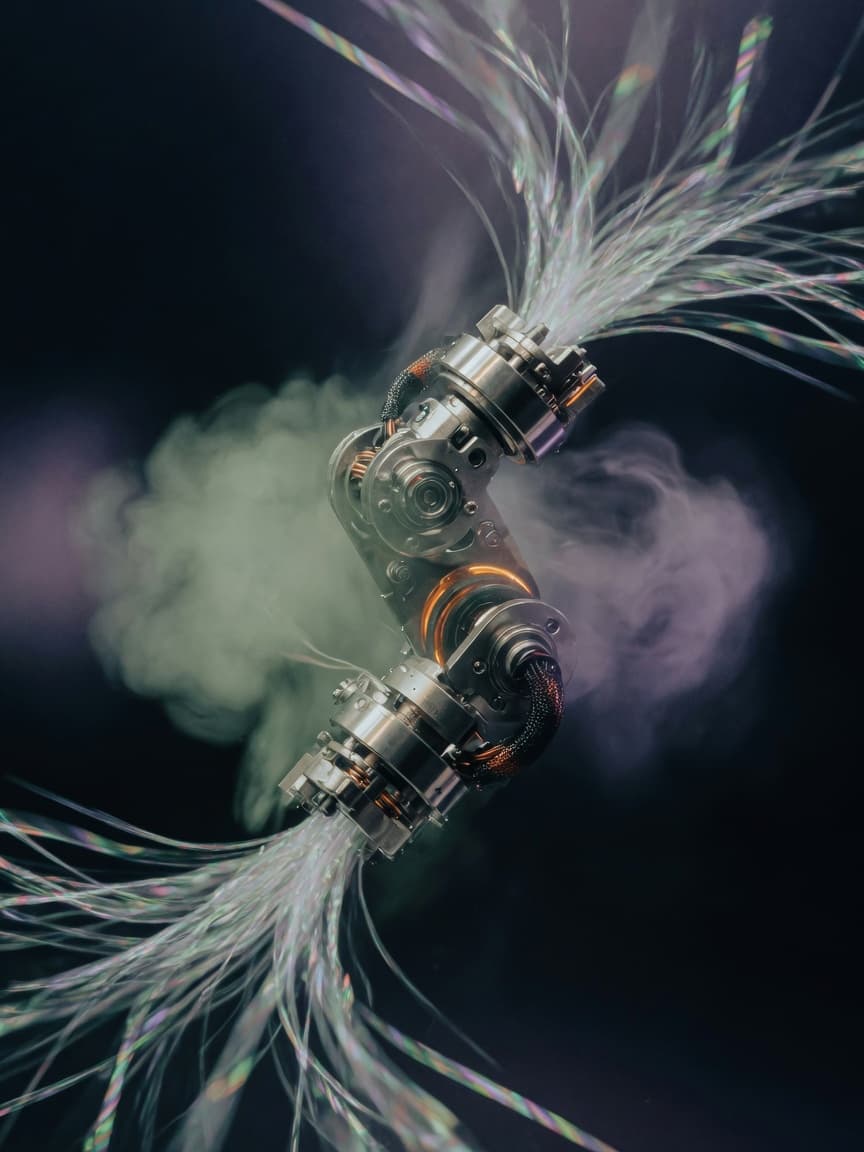

The most consequential bottleneck in humanoid robotics isn't the foundation model giving the robot its orders. It's the small, hot, brutally precise electromechanical module sitting at the shoulder, hip, and knee — the actuator — converting electrical current into controlled torque. Everything else is software. Actuators are physics.

And right now, whoever locks up actuator supply is positioning to own the guts of a market that Morgan Stanley pegs at $5 trillion and RBC has gone further, calling $9 trillion by the mid-2030s. Those numbers are almost certainly aspirational. The actuator math, however, is concrete: by most supply-chain estimates circulating in the industry, actuators account for 40 to 60 percent of a humanoid robot's total build cost. That single data point explains why CES 2026 felt less like a consumer electronics show and more like an industrial components expo.

LG's Appliance-to-Actuator Pivot

The headline move at CES this January was LG Electronics CEO Lyu Jae-cheol declaring 2026 the "inaugural year" of LG's humanoid robotics business and unveiling AXIUM — a branded line of robotic actuators designed for arms, legs, and hands. The pitch was blunt: LG manufactures roughly 45 million appliance motors annually. The thermal management, winding tolerances, and production lines that keep washing machine drums spinning at scale are, LG argues, directly transferable to robot joint modules.

LG Innotek's CEO has said meaningful external robotics revenue is still three to four years out. But the strategic intent is clear — LG Group is running what it internally brands "One LG," a cross-subsidiary sales motion that bundles actuators (LG Electronics), sensors (LG Innotek), and batteries (LG Energy Solution) into unified pitches for humanoid OEMs. It is, in other words, a vertical integration play dressed up as partnership.

The actuator layer is the new battery cell — whoever owns manufacturing scale owns margin.

The Actuation Wars: QDD vs. SEA vs. Planetary Roller Screw

Beneath the marketing, a genuine engineering fork is playing out across the major humanoid platforms. The legacy approach — high-ratio gearboxes mated to brushless DC motors — delivers precision but punishes robots when they fall or collide. You can't backdrive the joint; impacts transfer straight to the structure.

The field has evolved through two competing responses. Series Elastic Actuators (SEA) insert a calibrated spring element between the gearbox output and the load, storing impact energy and enabling force control without current-sensing tricks. Boston Dynamics built much of Atlas's dexterity on SEA principles before the electric pivot. The tradeoff is bandwidth — the spring limits how fast the joint can respond.

Quasi-Direct Drive (QDD) takes the opposite approach: low gear ratios (often 6:1 to 10:1 instead of 100:1+), high-torque density motors, and transparency as the core property. You can push on the joint and feel the motor resist naturally. MIT's Mini Cheetah popularized QDD for legged robots; Figure's early platform and Unitree's G1 lean heavily on this architecture. The tradeoff is thermal — low-ratio drives demand high continuous current, and heat is the enemy of uptime in a factory deployment.

Tesla, characteristically, chose neither cleanly. Optimus Gen 3 — which entered mass production at Fremont on January 21, 2026 — uses planetary roller screws for its primary linear actuation in the legs and spine. These are aerospace-grade components: expensive, stiff, and nearly zero-backlash. The hands are a different story: 50 actuators, 22 degrees of freedom, driven by tendons and miniaturized motors that borrow from what MinebeaMitsumi previewed at CES alongside Harmonic Drive Systems — tiny, high-torque units intended specifically for robotic finger actuation.

The Korean Supply Chain Bet

If LG is the loudest voice, it isn't alone. The quiet consensus in Seoul is that Korean conglomerates are better positioned than any other industrial bloc to dominate humanoid component supply chains — because they've spent decades building the manufacturing infrastructure for semiconductors, displays, and consumer appliances that maps almost directly to what robots need.

Hyundai Mobis is already shipping actuators to Boston Dynamics for Atlas. Samsung Electro-Mechanics is reportedly evaluating entry into the actuator market. MinebeaMitsumi — technically Japanese, but deeply integrated into Korean and Taiwanese supply chains — made its first-ever CES appearance this year specifically to surface its miniature motor work for robot hands.

The broader dynamic: humanoid OEMs (Tesla, Figure, Agility, Unitree, 1X) want to be robot companies, not motor companies. That creates genuine demand for Tier 1 actuator suppliers who can deliver at volume, with the thermal and torque specs the robot designers specify, at a cost that makes $30,000–$50,000 humanoids commercially viable for enterprise deployment.

The actuator market isn't a race to a single winner — it's fracturing by joint type, just like the auto drivetrain supplier world fractured by powertrain component.

What CVPR 2026 and the Research Frontier Are Watching

Academic robotics is tracking a longer arc that commercial platforms can't yet afford to bet on: compliant actuators built from electroactive polymers, pneumatic artificial muscles, and cable-driven architectures that can approximate the variable-stiffness behavior of biological muscle. These approaches offer safety profiles and power-to-weight ratios that rigid electric joints can't match — but manufacturing repeatability at scale remains unsolved.

The near-term research bet with commercial legs is on sensor-actuator integration: embedding torque, temperature, and proprioceptive sensing directly into the actuator module rather than bolting external sensors onto joints. The goal is latency. Every millisecond of round-trip between sensor and controller is a stability risk in a bipedal system. Integrated modules collapse that loop.

Smaller companies like Hebi Robotics and Odrive are shipping modular smart actuator packs — compute, sensing, and drive electronics in one housing — that are already showing up in research-to-deployment pipelines. The bet is that integrated actuator intelligence, not raw motor performance, becomes the differentiating spec by the time the humanoid market reaches scale deployments in 2027–2028.

The Real Constraint

The robot arms race of 2026 has a narrative problem: it's been almost entirely about the AI stack. Foundation models, imitation learning, policy networks, simulation-to-real pipelines. That framing is downstream of a much harder physical problem.

You can train a robot on a trillion robot-hours of synthetic data. But if the knee actuator overheats after four hours on a factory floor, if the finger joints lose torque at low temperature, if the harmonic drive wears at 10,000 cycles instead of 1,000,000 — the software doesn't matter. The actuator is the robot's immune system and its spine simultaneously.

The companies that figured this out first — the ones quietly building actuator roadmaps alongside their AI stacks, or locking supply agreements with LG and Hyundai Mobis before demand spikes — are playing a different game than the ones demoing impressive dexterous manipulation videos in controlled environments.

The muscle problem is real. And whoever solves it at scale won't just sell robots. They'll collect rent on every robot anyone else sells.